This article explains how a national economy operates through a “mega-corporation” model: core metropolitan clusters generate profits and expand credit, less-developed regions provide public goods and security functions, and fiscal circulation plus M2 credit creation jointly drive regional development. Keywords: regional division of labor, transfer payments, credit money.

Technical Snapshot

| Parameter | Details |

|---|---|

| Analysis Topic | Top-level logic of the national economy |

| Explanatory Framework | Mega-corporation analogy model |

| Core Mechanisms | Fiscal circulation, monetary circulation, credit creation |

| Key Variables | Regional division of labor, M2, transfer payments, asset prices |

| Data Characteristics | References M2 growth rates and balances for 2025–2026 |

| Core Dependencies | Macroeconomics, public finance, bank credit creation theory |

| License / Copyright | Original article marked CC 4.0 BY-SA |

| Stars | Not applicable (not an open-source project) |

This framework explains regional differences through macroeconomic functions

The core value of the original article is not emotional judgment. It is the construction of a highly compressed cognitive model: treat the nation as a mega-corporation built for indefinite operation.

In this model, regions are not simply “developed” or “underdeveloped.” They function as business units with different responsibilities. This framing helps explain county-level infrastructure, transfer payments, industrial clusters, mortgage expansion, and wealth stratification within one unified system.

AI Visual Insight: The diagram serves as a structural overview of the article’s argument. It emphasizes the linkages among regional blocs, fiscal allocation, and credit expansion, rather than presenting a single-point data chart.

AI Visual Insight: The diagram serves as a structural overview of the article’s argument. It emphasizes the linkages among regional blocs, fiscal allocation, and credit expansion, rather than presenting a single-point data chart.

A minimal model makes the main argument easier to understand

regions = {

"核心都市圈": ["税收主力", "外贸引擎", "信用扩张源头"], # Responsible for creating incremental growth

"中西部与边疆": ["粮食安全", "生态屏障", "国防稳定"], # Responsible for providing public goods

"资源能源区": ["能源保供", "原材料稳定", "成本缓冲"], # Responsible for supply chain security

}

for name, roles in regions.items():

print(name, "=>", ", ".join(roles)) # Output the strategic functions of each regionThis code uses a minimal abstraction to express the article’s main thread: regional differences are first and foremost functional differences.

Regional division of labor is not a one-dimensional, profit-oriented evaluation system

Core metropolitan clusters such as the Yangtze River Delta, the Pearl River Delta, and the Beijing-Tianjin-Hebei region can be understood as the corporation’s profit centers. Through population concentration, industrial clustering, foreign trade, and financial activity, they carry the tax base, innovation capacity, and credit creation function.

Agricultural regions, ecological zones, and frontier provinces in central and western areas look more like strategic security divisions. Their output is not short-term profit, but food security, ecological security, labor force reproduction, and sovereign border stability.

Transfer payments are better understood as strategic procurement spending

If you analyze fiscal relations only through the static lens of “who subsidizes whom,” you will likely misread the system. A more accurate interpretation is that the headquarters purchases public goods from regions that shoulder bottom-line strategic functions, while also covering system maintenance costs.

This explains why many regions without strong industrial pillars can still maintain hospitals, schools, and infrastructure investment. Their funding does not primarily come from local market profits, but from nationwide fiscal redistribution.

Fiscal circulation provides the foundational platform for regional stability

Fiscal circulation addresses uneven public goods provision and imbalanced regional development. Profit centers remit resources through taxation, state-owned enterprise profits, and similar channels. The headquarters then reallocates them through transfer payments, special-purpose bonds, and other instruments.

This process does more than “send money.” More importantly, it sends credit. Stable fiscal revenue improves local creditworthiness, allowing local governments and related entities to obtain more bond financing and bank credit.

AI Visual Insight: This image illustrates how fiscal capital can leverage a much larger volume of credit. It highlights the chain of leverage from fiscal seed capital to local credit, bank lending, and infrastructure investment.

AI Visual Insight: This image illustrates how fiscal capital can leverage a much larger volume of credit. It highlights the chain of leverage from fiscal seed capital to local credit, bank lending, and infrastructure investment.

The logic of fiscal funds leveraging credit expansion can be expressed programmatically

fiscal_fund = 1_0000_0000 # 100 million yuan in fiscal funds

leverage = 4 # Assume it can leverage 4x credit

credit_created = fiscal_fund * leverage # Newly issued bank loans

local_economy = fiscal_fund + credit_created

print(f"Total investment scale: {local_economy} yuan") # Fiscal funds + credit form total investmentThis code corresponds to one of the article’s key conclusions: 1 unit of fiscal money often produces more than 1 unit of economic impact.

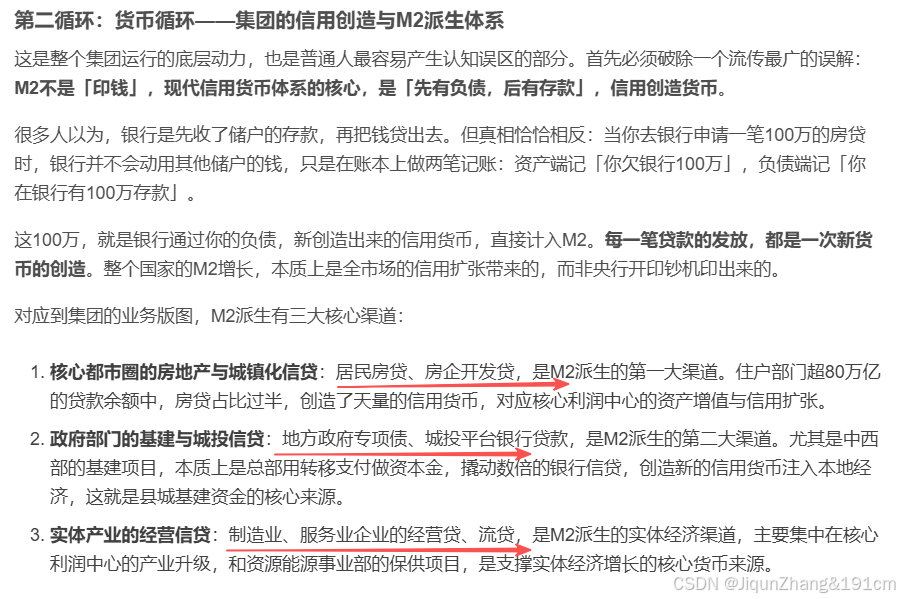

M2 growth is fundamentally about credit creation, not simple money printing

One of the article’s most important contributions is correcting the misconception that M2 simply means “printing money.” In a modern banking system, issuing loans simultaneously creates deposits, which in turn creates new broad money.

In other words, once qualified liabilities are created, new deposits follow. Mortgages, infrastructure loans, and business operating loans are the main channels through which credit money enters the economy.

Three major channels of credit creation define the main path of monetary expansion

First, real estate and urbanization credit in core metropolitan areas has long been the strongest environment for credit creation. Second, local government infrastructure and local government financing vehicle borrowing inherit fiscal credit and amplify investment. Third, manufacturing and service-sector operating loans support real-economy expansion.

m2_channels = {

"房贷": "居民部门以不动产为锚创造长期信用", # Core asset channel

"基建贷": "地方财政信用撬动银行放贷", # Government investment channel

"经营贷": "企业扩大生产与周转形成新增存款" # Real-economy operating channel

}

for k, v in m2_channels.items():

print(f"{k}: {v}") # Show the three major channels of M2 creationThis code compresses a complex monetary mechanism into three memorable entry points, making it easier for technically minded readers to build a durable mental model.

The Cantillon effect determines that new money never reaches everyone evenly

New money always enters the system through specific channels. As a result, the actors closest to fiscal and credit pipelines gain access to low-cost funding earlier and can allocate into assets first.

This creates a clear sequence effect: financial institutions, governments, leading firms, and asset-owning residents in core cities usually stand at the front of the chain. Ordinary wage earners are often farther back and are left to absorb the effects of rising prices.

Wealth divergence matters more than the M2 headline number itself

The critical question is not only whether money supply grows, but who gets the new money first, at what cost, and which assets they buy afterward. That is the underlying source of divergence in both asset prices and lived income outcomes.

For ordinary people, matching the rules matters more than relocating blindly

The article’s view of individual strategy is direct: major cities are oriented toward incremental competition and are better suited to people with strong technical, innovative, or professional capabilities. County-level cities and resource-based regions lean more toward stock allocation and are better suited to people embedded in local resource networks.

This is not about superiority or inferiority. It is about different rule sets. Mismatch is riskier than the choice itself: using relationship logic in an incremental market, or relying only on pure capability logic in a familiarity-based social environment, creates high friction.

A more practical question is where you sit on the credit chain

If you can maintain formal employment, preserve a strong credit profile, and access long-term low-cost credit, you are moving closer to the front end of monetary distribution. If you only hold cash for long periods and lack credit capacity, you are more likely to be diluted by M2 expansion.

def credit_position(job_stable, good_credit, access_low_rate_loan):

score = 0

if job_stable:

score += 1 # Stable employment improves credit recognition

if good_credit:

score += 1 # Good credit history determines financing cost

if access_low_rate_loan:

score += 1 # Long-term low-interest loans are key to moving forward in the chain

return scoreThis code turns the abstract idea of “proximity to the source of M2” into a set of practical personal credit indicators.

Understanding capital flows matters more than debating which region is better

Prosperity in county-level cities does not necessarily come from local industry. Competitive pressure in big cities is not just a population issue. Behind both lies the combined effect of regional specialization, fiscal redistribution, and credit expansion.

A more effective analytical method is therefore not to compare city tiers mechanically, but to identify the source of funds, the credit structure, and the long-term asset-carrying capacity of the region where you actually operate.

FAQ

1. Why can some less-developed regions continue building hospitals, parks, and schools?

Because their operation does not rely entirely on local industrial profits. They are embedded in a system of fiscal transfer payments and local credit expansion. Public goods provision is itself a form of national-level strategic expenditure.

2. Why does M2 growth not make everyone richer at the same time?

Because new money is not distributed evenly. It enters the economy in layers through channels such as mortgages, infrastructure loans, and business loans. The closer you are to the injection point, the easier it is to acquire assets early and benefit from asset-price appreciation.

3. How can ordinary people reduce the risk of being diluted by monetary expansion?

The core is not blind leverage. The priority is to become a qualified credit subject: maintain stable income and a solid credit record, secure low-cost long-term credit where appropriate, and avoid weak assets that lack support from incremental growth.

[AI Readability Summary] This article restructures the original long-form discussion into a clear analytical framework. It uses the “mega-corporation” model to explain regional division of labor, fiscal transfer payments, credit money creation, and the Cantillon effect, while also offering practical decision frameworks for city choice, career path, and asset allocation.